Custom MMM with ROAS Parameterization#

This notebook demonstrates how to build a custom Media Mix Model (MMM) parameterized by ROAS (Return on Ad Spend) instead of the classical regression (beta) coefficients. The technique is based on the paper Media Mix Model Calibration With Bayesian Priors by Zhang et al. (2024) and the simulation study Media Mix Model and Experimental Calibration by Juan Orduz.

Motivation#

In practice, MMMs suffer from omitted variable bias (unobserved confounders) which leads to biased channel contribution and ROAS estimates. Running randomized experiments (lift tests) can provide unbiased ROAS estimates for individual channels. The key idea in this notebook is to reparameterize the model so that the channel scaling coefficient \(\beta\) is expressed in terms of ROAS:

where \(x_{m,t}\) is the raw spend for channel \(m\) at time \(t\), and \(f_m\) is the adstock + saturation transformation. This allows injecting experimental ROAS estimates directly as Bayesian priors, partially correcting for confounding bias.

This is a different approach to the one taken in Case Study: Unobserved Confounders, ROAS and Lift Tests, where the ROAS is not a parameter of the model, but a derived quantity from the beta coefficients after lift-test calibration using the saturation-curve method (see Lift Test Calibration). The benefit of PyMC-Marketing’s calibration method is that the more experiments are conducted, the more precise the ROAS estimates become. In contrast, the approach here is more “static” in the sense that it uses an aggregation (e.g. mean or median) of ROAS estimates from experiments. We are losing information this way. Nevertheless, it is a clever and convenient parametrization that also works well in practice 🙂. The purpose of this notebook is to illustrate how PyMC-Marketing’s components can be used to build custom models, and how the ROAS parameterization works.

Approach#

We consider the same example as in the case study Case Study: Unobserved Confounders, ROAS and Lift Tests, where we have one unobserved confounder \(z\) that affects both channel \(x_1\) spend and the target \(y\). In this notebook, we compare two custom PyMC models:

Baseline model (

model_baseline): Standard beta-coefficient priors, no confounder \(z\) in the model. This demonstrates the bias from omitted variables.Calibrated model (

model_calibrated): ROAS priors from “experiments” replace beta priors. Same structure, still no \(z\), but ROAS priors mitigate the bias.

We use PyMC-Marketing components (GeometricAdstock, YearlyFourier) alongside raw PyMC for maximum flexibility.

See also

Case Study: Unobserved Confounders, ROAS and Lift Tests for the full 3-model comparison using lift-test calibration.

Custom Models with MMM components and Custom Geo-Hierarchical MMM with Splines for other custom model examples.

Lift Test Calibration for the lift-test likelihood approach to calibration.

Prepare Notebook#

import arviz as az

import graphviz as gr

import matplotlib.pyplot as plt

import matplotlib.ticker as mtick

import numpy as np

import pandas as pd

import preliz as pz

import pymc as pm

import seaborn as sns

import xarray as xr

from pymc_extras.prior import Prior

from sklearn.preprocessing import MaxAbsScaler

from pymc_marketing.mmm import GeometricAdstock

from pymc_marketing.mmm.fourier import YearlyFourier

from pymc_marketing.mmm.transformers import logistic_saturation

from pymc_marketing.paths import data_dir

az.style.use("arviz-darkgrid")

plt.rcParams["figure.figsize"] = [12, 7]

plt.rcParams["figure.dpi"] = 100

plt.rcParams["figure.facecolor"] = "white"

%load_ext autoreload

%autoreload 2

%config InlineBackend.figure_format = "retina"

seed: int = sum(map(ord, "mmm"))

rng: np.random.Generator = np.random.default_rng(seed=seed)

Load and Explore Data#

We use the same synthetic dataset from Case Study: Unobserved Confounders, ROAS and Lift Tests. It was generated with an unobserved confounder \(z\) that causally affects both channel \(x_1\) spend and the target \(y\) (for more details on the data generating process, see the original blog post Media Mix Modeling with PyMC-Marketing). The dataset includes ground-truth columns (y01 and y02) representing potential outcomes when each channel is turned off, which we use to compute the true ROAS.

data_path = data_dir / "mmm_roas_data.csv"

raw_df = pd.read_csv(data_path, parse_dates=["date"])

raw_df.info()

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 131 entries, 0 to 130

Data columns (total 20 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 date 131 non-null datetime64[ns]

1 dayofyear 131 non-null int64

2 quarter 131 non-null object

3 trend 131 non-null float64

4 cs 131 non-null float64

5 cc 131 non-null float64

6 seasonality 131 non-null float64

7 z 131 non-null float64

8 x1 131 non-null float64

9 x2 131 non-null float64

10 epsilon 131 non-null float64

11 x1_adstock 131 non-null float64

12 x2_adstock 131 non-null float64

13 x1_adstock_saturated 131 non-null float64

14 x2_adstock_saturated 131 non-null float64

15 x1_effect 131 non-null float64

16 x2_effect 131 non-null float64

17 y 131 non-null float64

18 y01 131 non-null float64

19 y02 131 non-null float64

dtypes: datetime64[ns](1), float64(17), int64(1), object(1)

memory usage: 20.6+ KB

Causal DAG#

The data generating process follows this causal structure. Note the confounder \(z\) affecting both \(x_1\) and \(y\):

g = gr.Digraph()

g.node(name="seasonality", label="seasonality", color="lightgray", style="filled")

g.node(name="trend", label="trend")

g.node(name="z", label="z (unobserved)", color="lightgray", style="filled")

g.node(name="x1", label="x1", color="#2a2eec80", style="filled")

g.node(name="x2", label="x2", color="#fa7c1780", style="filled")

g.node(name="y", label="y", color="#328c0680", style="filled")

g.edge(tail_name="seasonality", head_name="x1")

g.edge(tail_name="z", head_name="x1")

g.edge(tail_name="x1", head_name="y")

g.edge(tail_name="seasonality", head_name="y")

g.edge(tail_name="trend", head_name="y")

g.edge(tail_name="z", head_name="y")

g.edge(tail_name="x2", head_name="y")

g

Since \(z\) is unobserved, we cannot include it in the model. This means the backdoor path \(x_1 \leftarrow z \rightarrow y\) remains open, leading to omitted variable bias in the estimate of \(x_1\)’s effect.

Select Modeling Columns#

For modeling, we only use date, dayofyear, x1, x2, and y, deliberately excluding \(z\) to simulate a realistic scenario.

channels = ["x1", "x2"]

target = "y"

model_df = raw_df.filter(["date", "dayofyear", *channels, target])

model_df.head()

| date | dayofyear | x1 | x2 | y | |

|---|---|---|---|---|---|

| 0 | 2021-10-02 | 275 | 0.646554 | 0.336188 | 199.329637 |

| 1 | 2021-10-09 | 282 | 1.411917 | 0.203931 | 371.237041 |

| 2 | 2021-10-16 | 289 | 0.837610 | 0.024026 | 272.215933 |

| 3 | 2021-10-23 | 296 | 0.973612 | 0.120257 | 291.104040 |

| 4 | 2021-10-30 | 303 | 1.415985 | 0.084630 | 386.243000 |

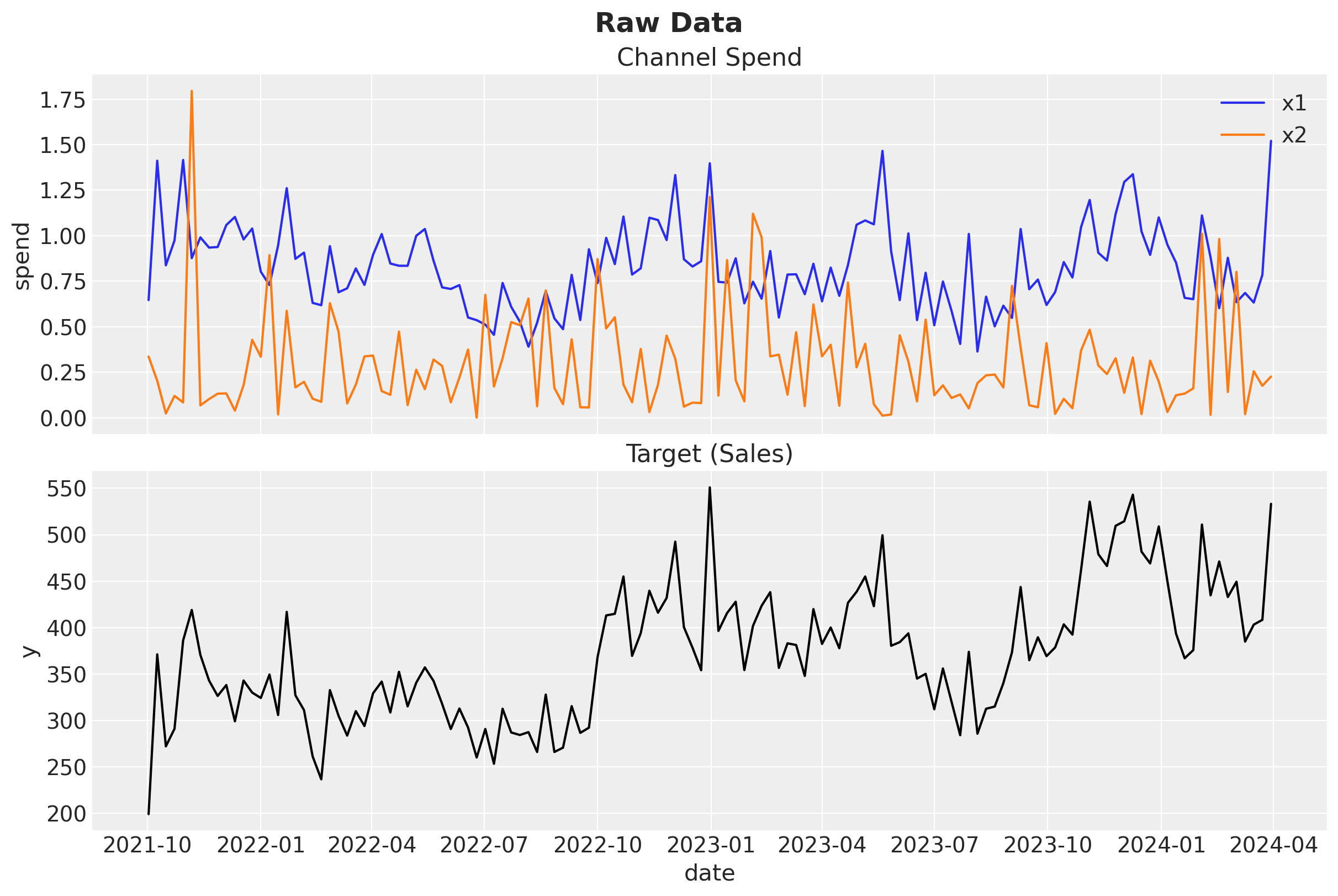

fig, ax = plt.subplots(

nrows=2,

ncols=1,

figsize=(12, 8),

sharex=True,

layout="constrained",

)

for i, ch in enumerate(channels):

sns.lineplot(data=model_df, x="date", y=ch, color=f"C{i}", label=ch, ax=ax[0])

ax[0].legend(loc="upper right")

ax[0].set(ylabel="spend", title="Channel Spend")

sns.lineplot(data=model_df, x="date", y=target, color="black", ax=ax[1])

ax[1].set(ylabel=target, title="Target (Sales)")

fig.suptitle("Raw Data", fontsize=18, fontweight="bold");

True ROAS (Ground Truth)#

The dataset contains potential outcome columns y01 (sales without \(x_1\)) and y02 (sales without \(x_2\)). We compute the true global ROAS as:

roas_true_x1 = (raw_df["y"] - raw_df["y01"]).sum() / raw_df["x1"].sum()

roas_true_x2 = (raw_df["y"] - raw_df["y02"]).sum() / raw_df["x2"].sum()

print(f"True ROAS x1: {roas_true_x1:.2f}")

print(f"True ROAS x2: {roas_true_x2:.2f}")

True ROAS x1: 93.39

True ROAS x2: 171.41

Data Preparation and Scaling#

We scale the data using MaxAbsScaler to improve sampling efficiency (we could also do the scaling manually but this shows how to integrate PyMC posterior distributions with scikit-learn transformers). The time index, target, and channels are each scaled independently.

date = model_df["date"]

dayofyear = model_df["dayofyear"].to_numpy()

index_scaler = MaxAbsScaler()

index_scaled = index_scaler.fit_transform(

model_df.reset_index(drop=False)[["index"]]

).flatten()

target_scaler = MaxAbsScaler()

target_scaled = target_scaler.fit_transform(model_df[[target]]).flatten()

channels_scaler = MaxAbsScaler()

channels_scaled = channels_scaler.fit_transform(model_df[channels])

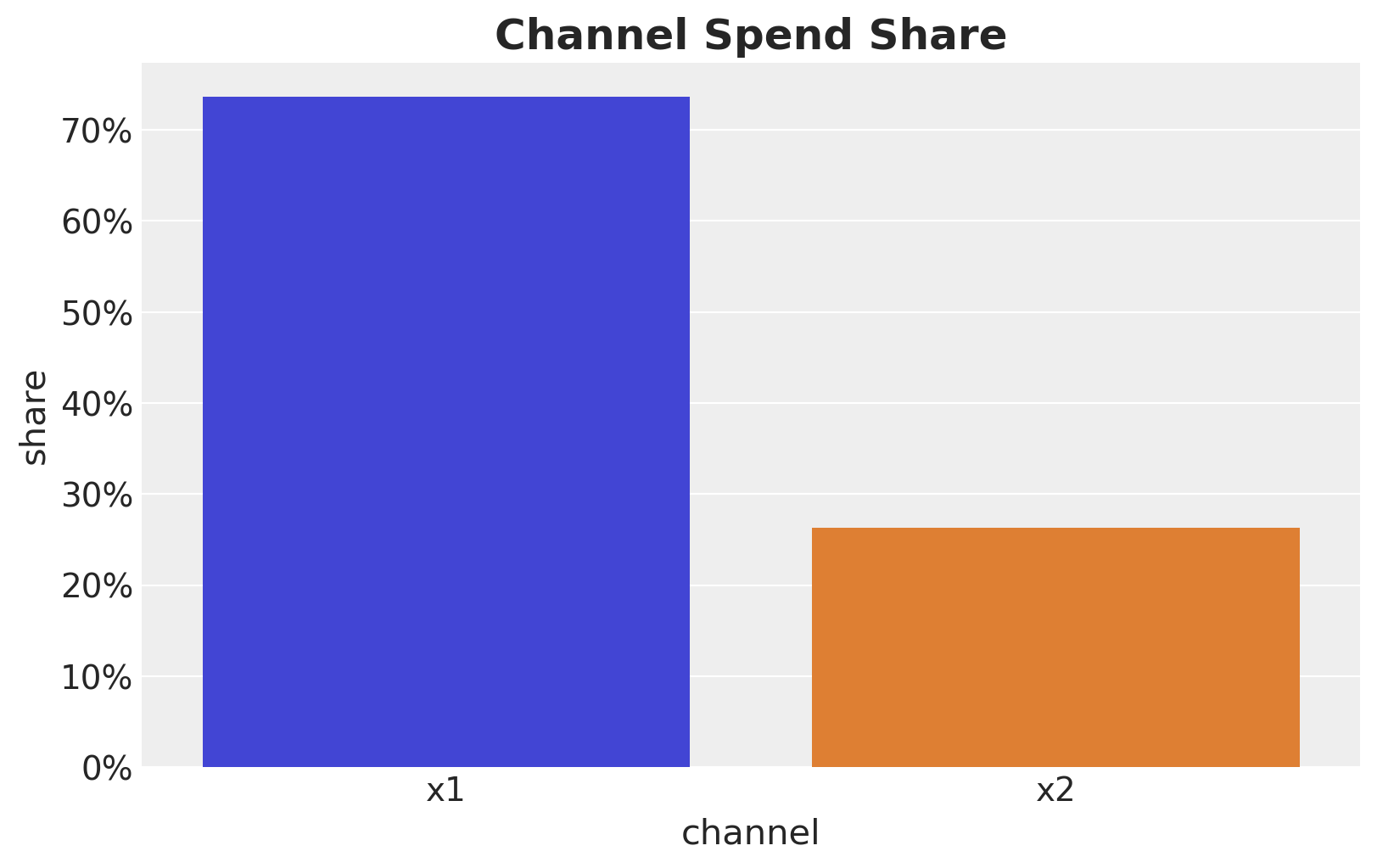

Let’s look into the channel spend share:

channel_share = raw_df[channels].sum() / raw_df[channels].sum().sum()

fig, ax = plt.subplots(figsize=(8, 5))

sns.barplot(

x=channel_share.index, y=channel_share.values, hue=channel_share.index, ax=ax

)

ax.yaxis.set_major_formatter(mtick.PercentFormatter(xmax=1))

ax.set(xlabel="channel", ylabel="share")

ax.set_title("Channel Spend Share", fontsize=18, fontweight="bold");

Model Components Setup#

We define reusable PyMC-Marketing components for adstock and seasonality. For the saturation transform, we use the raw logistic_saturation function (without the LogisticSaturation class) because we need to handle the channel scaling coefficient \(\beta\) separately in each model: the baseline uses a direct prior, while the calibrated model derives it from ROAS.

l_max = 4

adstock = GeometricAdstock(

l_max=l_max,

normalize=True,

priors={"alpha": Prior("Beta", alpha=2, beta=3, dims="channel")},

)

yearly_fourier = YearlyFourier(

n_order=3,

prior=Prior("Normal", mu=0, sigma=1, dims="fourier"),

)

Baseline Model: Standard Beta Priors (No Confounder)#

This model excludes the confounder \(z\) and uses standard HalfNormal priors on beta_channel, weighted by each channel’s spend share. We expect the ROAS of \(x_1\) to be heavily overestimated due to the open backdoor path through \(z\).

Tip

We will add a time-varying intercept using a Hilbert Space Gaussian Process. For details on the choice of priors, see the original blog post Media Mix Modeling with PyMC-Marketing and the PyMC example Gaussian Processes: HSGP Reference & First Steps.

coords = {"date": date, "channel": channels}

with pm.Model(coords=coords) as model_baseline:

# --- Data Containers ---

index_data = pm.Data("index_scaled", index_scaled, dims="date")

channels_data = pm.Data(

"channels_scaled", channels_scaled, dims=("date", "channel")

)

y_data = pm.Data("y_scaled", target_scaled, dims="date")

# --- HSGP Trend ---

amplitude_trend = pm.HalfNormal("amplitude_trend", sigma=1)

ls_trend = pz.maxent(

distribution=pz.InverseGamma(),

lower=0.1,

upper=0.9,

mass=0.95,

plot=False,

).to_pymc("ls_trend")

cov_trend = amplitude_trend * pm.gp.cov.ExpQuad(input_dim=1, ls=ls_trend)

gp_trend = pm.gp.HSGP(m=[20], c=1.5, cov_func=cov_trend)

f_trend = gp_trend.prior("f_trend", X=index_data[:, None], dims="date")

# --- Channel Effects ---

lam = pm.Gamma("lam", alpha=2, beta=2, dims="channel")

beta_channel = pm.HalfNormal(

"beta_channel", sigma=channel_share.to_numpy(), dims="channel"

)

adstocked = adstock.apply(channels_data, dims="channel")

channel_adstock_saturated = pm.Deterministic(

"channel_adstock_saturated",

logistic_saturation(adstocked, lam=lam),

dims=("date", "channel"),

)

channel_contributions = pm.Deterministic(

"channel_contributions",

channel_adstock_saturated * beta_channel,

dims=("date", "channel"),

)

# --- Seasonality ---

fourier_contribution = pm.Deterministic(

"fourier_contribution",

yearly_fourier.apply(dayofyear),

dims="date",

)

# --- Mean ---

mu = pm.Deterministic(

"mu",

f_trend + channel_contributions.sum(axis=-1) + fourier_contribution,

dims="date",

)

# --- Likelihood ---

sigma = pm.HalfNormal("sigma", sigma=1)

nu = pm.Gamma("nu", alpha=25, beta=2)

pm.StudentT("y", nu=nu, mu=mu, sigma=sigma, observed=y_data, dims="date")

pm.model_to_graphviz(model_baseline)

Fit Model#

with model_baseline:

idata_baseline = pm.sample(

target_accept=0.95,

tune=1_500,

draws=1_000,

chains=4,

nuts_sampler="nutpie",

random_seed=rng,

)

posterior_predictive_baseline = pm.sample_posterior_predictive(

trace=idata_baseline, random_seed=rng

)

Sampler Progress

Total Chains: 4

Active Chains: 0

Finished Chains: 4

Sampling for 12 seconds

Estimated Time to Completion: now

| Progress | Draws | Divergences | Step Size | Gradients/Draw |

|---|---|---|---|---|

| 2500 | 0 | 0.06 | 63 | |

| 2500 | 0 | 0.06 | 383 | |

| 2500 | 0 | 0.07 | 63 | |

| 2500 | 0 | 0.06 | 63 |

Sampling: [y]

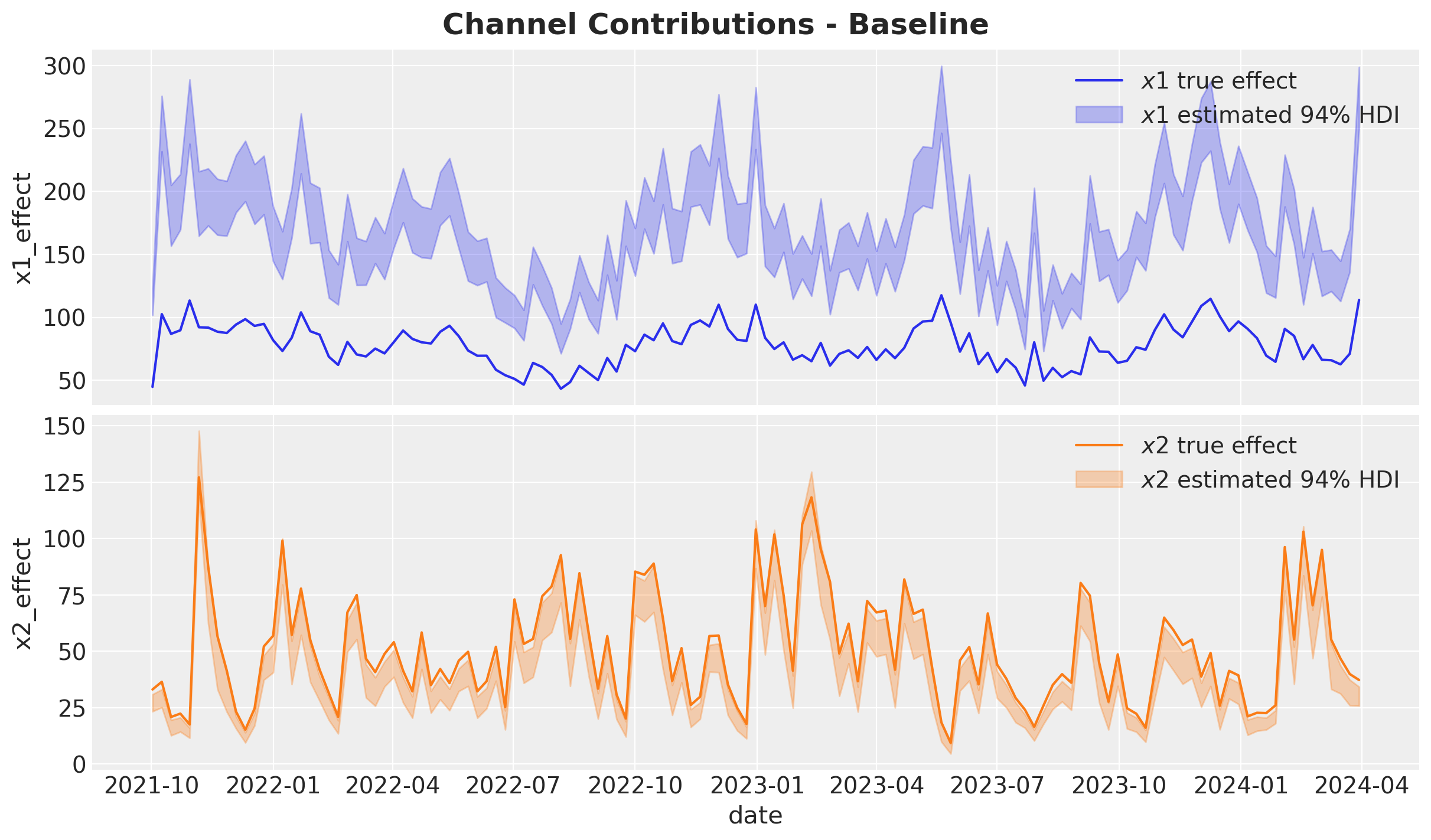

Channel Contributions vs True Effects#

We compare estimated channel contributions against the ground truth. The omitted confounder \(z\) causes \(x_1\)’s contribution to be heavily overestimated.

First, let’s do some proper scaling back to the original data.

pp_mu_baseline = xr.apply_ufunc(

target_scaler.inverse_transform,

idata_baseline["posterior"]["mu"].expand_dims(dim={"_": 1}, axis=-1),

input_core_dims=[["date", "_"]],

output_core_dims=[["date", "_"]],

vectorize=True,

).squeeze(dim="_")

pp_contributions_baseline = xr.apply_ufunc(

target_scaler.inverse_transform,

idata_baseline["posterior"]["channel_contributions"],

input_core_dims=[["date", "channel"]],

output_core_dims=[["date", "channel"]],

vectorize=True,

)

Now we can plot the estimated channel contributions against the true effects.

amplitude = 100

fig, ax = plt.subplots(

nrows=2, ncols=1, figsize=(12, 7), sharex=True, layout="constrained"

)

for i, ch in enumerate(channels):

sns.lineplot(

x="date",

y=f"{ch}_effect",

data=raw_df.assign(

**{f"{ch}_effect": lambda df, c=ch: amplitude * df[f"{c}_effect"]}

),

color=f"C{i}",

label=rf"${ch}$ true effect",

ax=ax[i],

)

az.plot_hdi(

x=date,

y=pp_contributions_baseline.sel(channel=ch),

hdi_prob=0.94,

color=f"C{i}",

fill_kwargs={"alpha": 0.3, "label": rf"${ch}$ estimated $94\%$ HDI"},

smooth=False,

ax=ax[i],

)

ax[i].legend(loc="upper right")

fig.suptitle("Channel Contributions - Baseline", fontsize=18, fontweight="bold");

We clearly see the confounding bias from the omitted variable \(z\) in the \(x_1\) contribution estimation. Let’s see how this bias gets translated into ROAS.

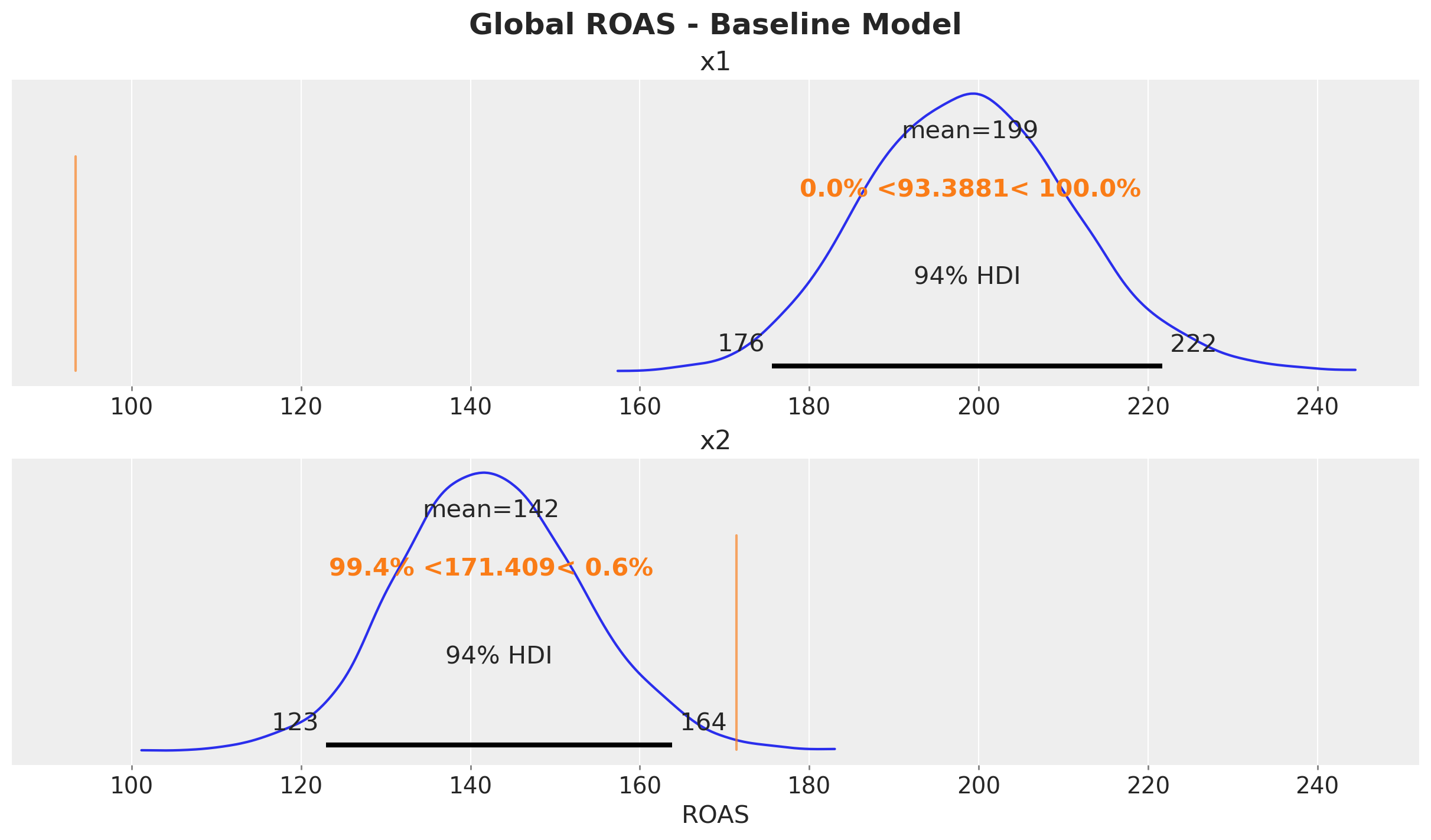

ROAS Estimation (Baseline)#

We compute the global ROAS by generating counterfactual predictions with each channel set to zero.

predictions_roas_baseline = {}

for channel in channels:

with model_baseline:

pm.set_data(

new_data={

"channels_scaled": channels_scaler.transform(

raw_df[channels].assign(**{channel: 0})

)

}

)

preds = pm.sample_posterior_predictive(

trace=idata_baseline,

var_names=["mu"],

progressbar=False,

random_seed=rng,

)

mu_counterfactual = xr.apply_ufunc(

target_scaler.inverse_transform,

preds["posterior_predictive"]["mu"].expand_dims(dim={"_": 1}, axis=-1),

input_core_dims=[["date", "_"]],

output_core_dims=[["date", "_"]],

vectorize=True,

).squeeze(dim="_")

diff = pp_mu_baseline - mu_counterfactual

predictions_roas_baseline[channel] = diff.sum(dim="date") / raw_df[channel].sum()

Sampling: []

Sampling: []

Let’s visualize the results.

fig, ax = plt.subplots(

nrows=2, ncols=1, figsize=(12, 7), sharex=True, layout="constrained"

)

az.plot_posterior(predictions_roas_baseline["x1"], ref_val=roas_true_x1, ax=ax[0])

ax[0].set(title="x1")

az.plot_posterior(predictions_roas_baseline["x2"], ref_val=roas_true_x2, ax=ax[1])

ax[1].set(title="x2", xlabel="ROAS")

fig.suptitle("Global ROAS - Baseline Model", fontsize=18, fontweight="bold");

The baseline model massively overestimates the ROAS of \(x_1\) due to the confounding bias from the omitted variable \(z\). This is something we already know from the case study Case Study: Unobserved Confounders, ROAS and Lift Tests.

Calibrated Model: ROAS Parameterization#

We now build the same model structure but replace the beta_channel prior with a derived quantity based on ROAS priors. The ROAS values come from hypothetical experiments that provide unbiased estimates close to the true values.

Experiment Calibration#

Suppose experiments yielded the following ROAS estimates:

roas_x1_bar = 95

roas_x2_bar = 170

roas_x1_bar_scaled = roas_x1_bar / target_scaler.scale_.item()

roas_x2_bar_scaled = roas_x2_bar / target_scaler.scale_.item()

roas_bar_scaled = np.array([roas_x1_bar_scaled, roas_x2_bar_scaled])

error = 30

error_scaled = error / target_scaler.scale_.item()

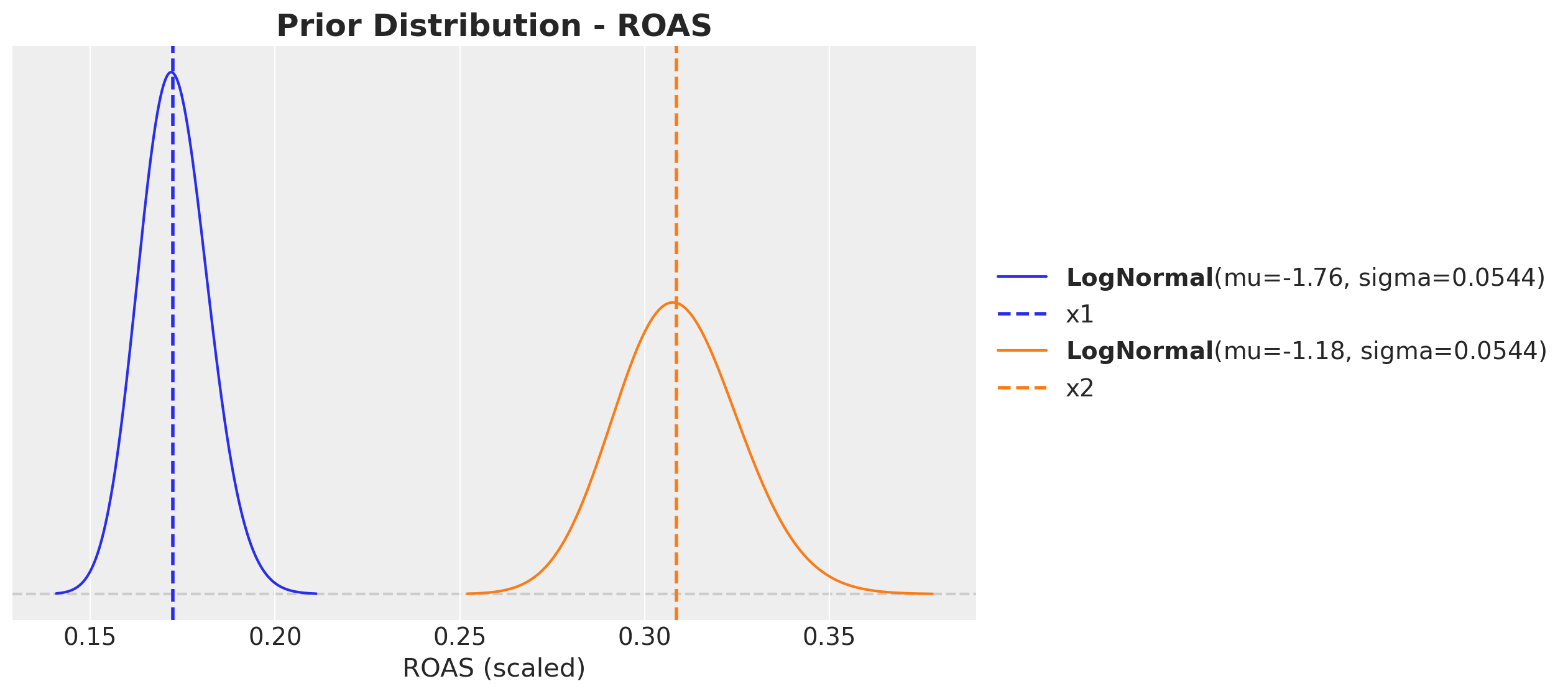

ROAS Prior Distributions#

We use LogNormal priors centered at the experimental ROAS estimates. The LogNormal ensures positivity and allows for right-skewed uncertainty.

fig, ax = plt.subplots(figsize=(10, 6))

pz.LogNormal(mu=np.log(roas_x1_bar_scaled), sigma=error_scaled).plot_pdf(

color="C0", ax=ax

)

ax.axvline(x=roas_x1_bar_scaled, color="C0", linestyle="--", linewidth=2, label="x1")

pz.LogNormal(mu=np.log(roas_x2_bar_scaled), sigma=error_scaled).plot_pdf(

color="C1", ax=ax

)

ax.axvline(x=roas_x2_bar_scaled, color="C1", linestyle="--", linewidth=2, label="x2")

ax.legend(loc="center left", bbox_to_anchor=(1, 0.5))

ax.set(xlabel="ROAS (scaled)")

ax.set_title("Prior Distribution - ROAS", fontsize=18, fontweight="bold");

Model Specification#

The key change from the baseline: instead of beta_channel ~ HalfNormal(...), we define roas ~ LogNormal(...) and derive beta_channel deterministically:

This ensures the total channel contribution equals ROAS * total_spend in expectation (the \(\epsilon\) term is a small constant to avoid division by zero).

eps = np.finfo(float).eps

with pm.Model(coords=coords) as model_calibrated:

# --- Data Containers ---

index_data = pm.Data("index_scaled", index_scaled, dims="date")

channels_data = pm.Data(

"channels_scaled", channels_scaled, dims=("date", "channel")

)

channels_cost_data = pm.Data(

"channels_cost", raw_df[channels].to_numpy(), dims=("date", "channel")

)

y_data = pm.Data("y_scaled", target_scaled, dims="date")

# --- HSGP Trend ---

amplitude_trend = pm.HalfNormal("amplitude_trend", sigma=1)

ls_trend = pz.maxent(

distribution=pz.InverseGamma(),

lower=0.1,

upper=0.9,

mass=0.95,

plot=False,

).to_pymc("ls_trend")

cov_trend = amplitude_trend * pm.gp.cov.ExpQuad(input_dim=1, ls=ls_trend)

gp_trend = pm.gp.HSGP(m=[20], c=1.5, cov_func=cov_trend)

f_trend = gp_trend.prior("f_trend", X=index_data[:, None], dims="date")

# --- Channel Effects (ROAS parameterization) ---

lam = pm.Gamma("lam", alpha=2, beta=2, dims="channel")

roas = pm.LogNormal(

"roas", mu=np.log(roas_bar_scaled), sigma=error_scaled, dims="channel"

)

adstocked = adstock.apply(channels_data, dims="channel")

channel_adstock_saturated = pm.Deterministic(

"channel_adstock_saturated",

logistic_saturation(adstocked, lam=lam),

dims=("date", "channel"),

)

beta_channel = pm.Deterministic(

"beta_channel",

(channels_cost_data.sum(axis=0) * roas)

/ (channel_adstock_saturated.sum(axis=0) + eps),

dims="channel",

)

channel_contributions = pm.Deterministic(

"channel_contributions",

channel_adstock_saturated * beta_channel,

dims=("date", "channel"),

)

# --- Seasonality ---

fourier_contribution = pm.Deterministic(

"fourier_contribution",

yearly_fourier.apply(dayofyear),

dims="date",

)

# --- Mean ---

mu = pm.Deterministic(

"mu",

f_trend + channel_contributions.sum(axis=-1) + fourier_contribution,

dims="date",

)

# --- Likelihood ---

sigma = pm.HalfNormal("sigma", sigma=1)

nu = pm.Gamma("nu", alpha=25, beta=2)

pm.StudentT("y", nu=nu, mu=mu, sigma=sigma, observed=y_data, dims="date")

pm.model_to_graphviz(model_calibrated)

Fit Model#

with model_calibrated:

idata_calibrated = pm.sample(

target_accept=0.95,

draws=1_000,

chains=4,

nuts_sampler="nutpie",

random_seed=rng,

)

posterior_predictive_calibrated = pm.sample_posterior_predictive(

trace=idata_calibrated, random_seed=rng

)

Sampler Progress

Total Chains: 4

Active Chains: 0

Finished Chains: 4

Sampling for now

Estimated Time to Completion: now

| Progress | Draws | Divergences | Step Size | Gradients/Draw |

|---|---|---|---|---|

| 2000 | 0 | 0.07 | 63 | |

| 2000 | 0 | 0.07 | 63 | |

| 2000 | 0 | 0.09 | 63 | |

| 2000 | 0 | 0.07 | 63 |

Sampling: [y]

We do not see any divergences.

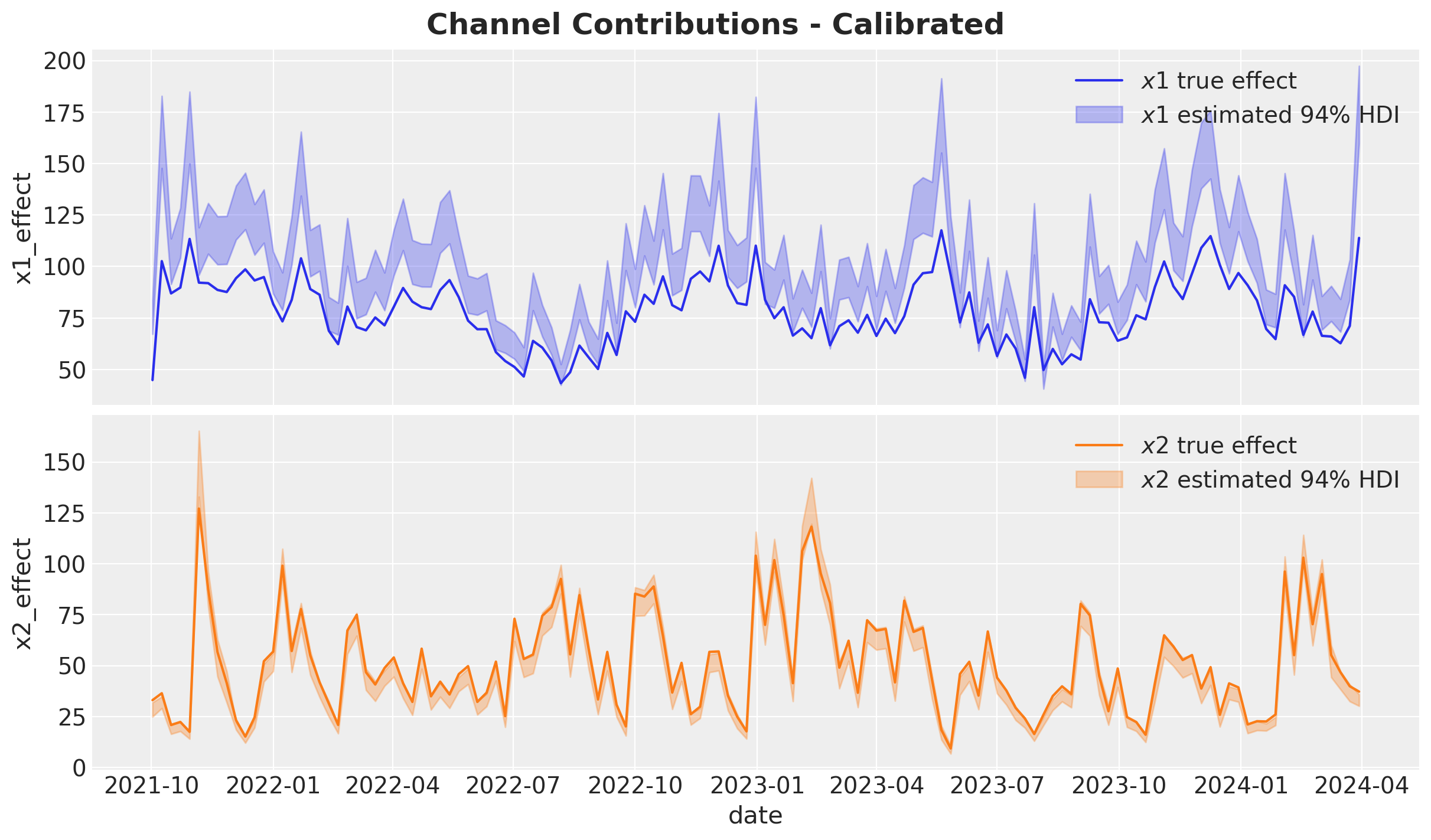

Channel Contributions vs True Effects#

As before, we scale back the estimated channel contributions to the original data.

pp_mu_calibrated = xr.apply_ufunc(

target_scaler.inverse_transform,

idata_calibrated["posterior"]["mu"].expand_dims(dim={"_": 1}, axis=-1),

input_core_dims=[["date", "_"]],

output_core_dims=[["date", "_"]],

vectorize=True,

).squeeze(dim="_")

pp_contributions_calibrated = xr.apply_ufunc(

target_scaler.inverse_transform,

idata_calibrated["posterior"]["channel_contributions"],

input_core_dims=[["date", "channel"]],

output_core_dims=[["date", "channel"]],

vectorize=True,

)

fig, ax = plt.subplots(

nrows=2, ncols=1, figsize=(12, 7), sharex=True, layout="constrained"

)

for i, ch in enumerate(channels):

sns.lineplot(

x="date",

y=f"{ch}_effect",

data=raw_df.assign(

**{f"{ch}_effect": lambda df, c=ch: amplitude * df[f"{c}_effect"]}

),

color=f"C{i}",

label=rf"${ch}$ true effect",

ax=ax[i],

)

az.plot_hdi(

x=date,

y=pp_contributions_calibrated.sel(channel=ch),

hdi_prob=0.94,

color=f"C{i}",

fill_kwargs={"alpha": 0.3, "label": rf"${ch}$ estimated $94\%$ HDI"},

smooth=False,

ax=ax[i],

)

ax[i].legend(loc="upper right")

fig.suptitle("Channel Contributions - Calibrated", fontsize=18, fontweight="bold");

The results are much better! The contributions are much closer to the true effects. It is not perfect for \(x_1\), but it is much better than before. This can translate into better decisions and downstream optimization.

ROAS Estimation (Calibrated)#

For the calibrated model, as before, we generate counterfactual predictions by zeroing out both channels_scaled (the model input) and channels_cost.

predictions_roas_calibrated = {}

for channel in channels:

with model_calibrated:

pm.set_data(

new_data={

"channels_scaled": channels_scaler.transform(

raw_df[channels].assign(**{channel: 0})

),

"channels_cost": raw_df[channels].assign(**{channel: 0}).to_numpy(),

}

)

preds = pm.sample_posterior_predictive(

trace=idata_calibrated,

var_names=["mu"],

progressbar=False,

random_seed=rng,

)

mu_counterfactual = xr.apply_ufunc(

target_scaler.inverse_transform,

preds["posterior_predictive"]["mu"].expand_dims(dim={"_": 1}, axis=-1),

input_core_dims=[["date", "_"]],

output_core_dims=[["date", "_"]],

vectorize=True,

).squeeze(dim="_")

diff = pp_mu_calibrated - mu_counterfactual

predictions_roas_calibrated[channel] = diff.sum(dim="date") / raw_df[channel].sum()

Sampling: []

Sampling: []

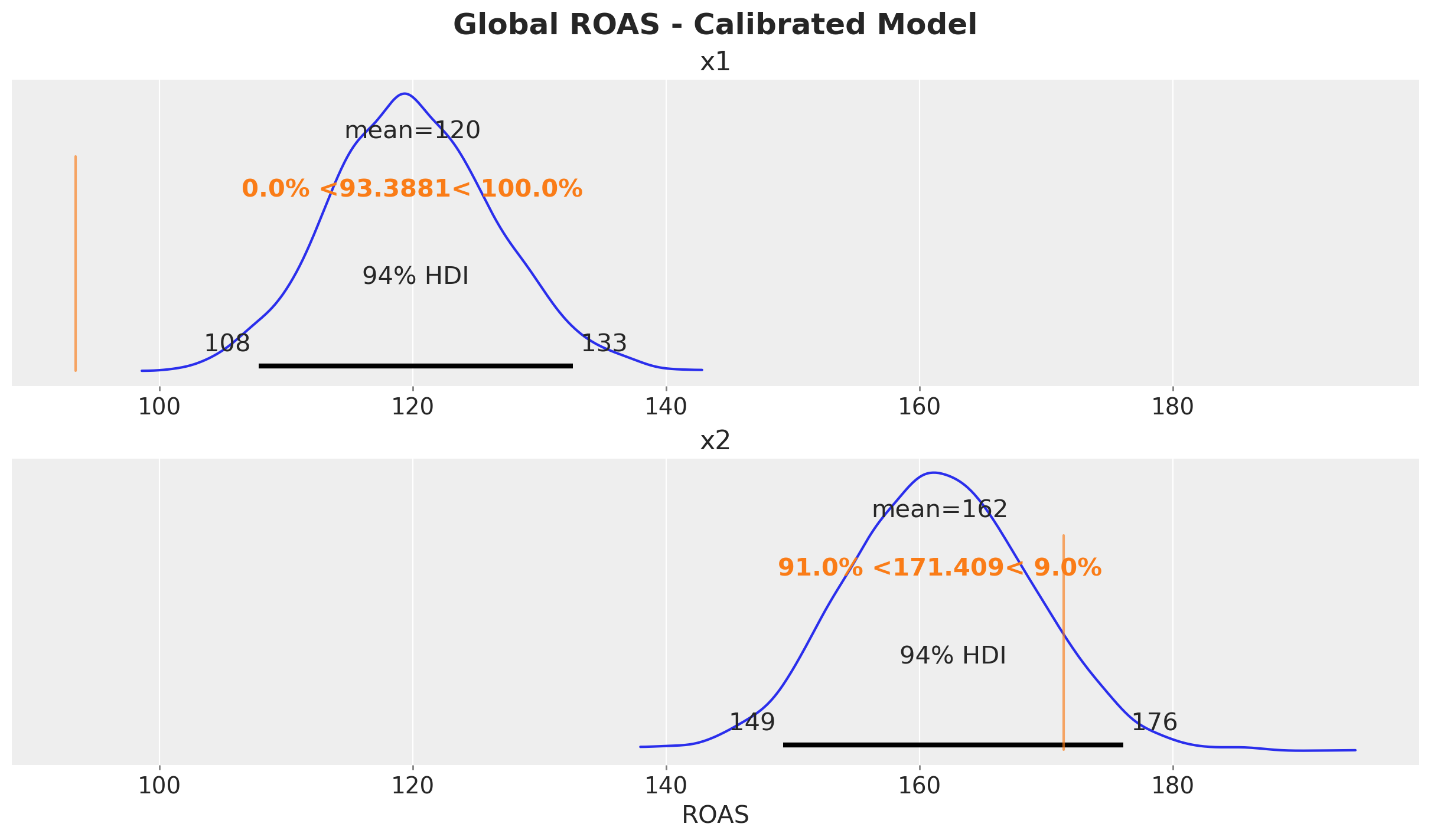

fig, ax = plt.subplots(

nrows=2, ncols=1, figsize=(12, 7), sharex=True, layout="constrained"

)

az.plot_posterior(predictions_roas_calibrated["x1"], ref_val=roas_true_x1, ax=ax[0])

ax[0].set(title="x1")

az.plot_posterior(predictions_roas_calibrated["x2"], ref_val=roas_true_x2, ax=ax[1])

ax[1].set(title="x2", xlabel="ROAS")

fig.suptitle("Global ROAS - Calibrated Model", fontsize=18, fontweight="bold");

The ROAS estimates are now closer to the true values, especially for \(x_1\) where the confounding bias was most severe. Directionally, these estimates are much better for decision-making.

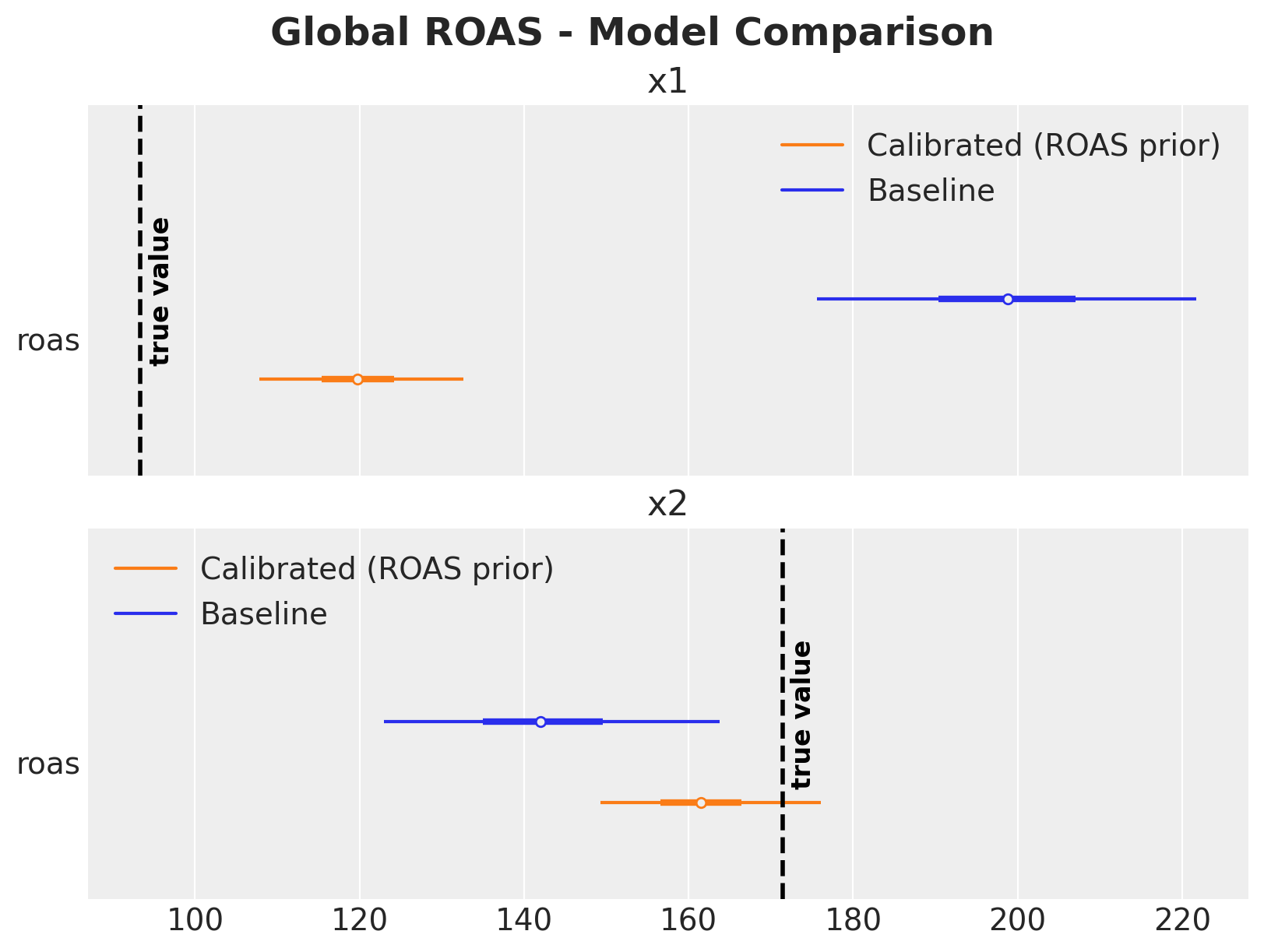

Model Comparison#

Let’s summarize the results in a single figure.

The comparison shows (as described above):

\(x_1\): The baseline model massively overestimates ROAS due to the confounding bias from \(z\). The calibrated model, informed by the experimental ROAS prior, brings the estimate much closer to the true value.

\(x_2\): Both models produce reasonable estimates since \(x_2\) has no confounding path, though the calibrated model provides tighter uncertainty bounds.

Note that the ROAS posteriors in the calibrated model are not identical to the priors; the likelihood (observed data) still influences the final estimates. The ROAS priors act as regularization, pulling the estimates toward experimentally validated values while still allowing the data to inform the posterior. This is where adding more experiments with additional likelihoods will help a lot (see Lift Test Calibration).

%load_ext watermark

%watermark -n -u -v -iv -w

Last updated: Wed, 04 Mar 2026

Python implementation: CPython

Python version : 3.13.12

IPython version : 9.10.0

arviz : 0.23.4

graphviz : 0.21

matplotlib : 3.10.8

numpy : 2.4.2

pandas : 2.3.3

preliz : 0.24.0

pymc : 5.28.1

pymc_extras : 0.9.1

pymc_marketing: 0.18.2

seaborn : 0.13.2

sklearn : 1.8.0

xarray : 2026.2.0

Watermark: 2.6.0